What is the first step of the accounting cycle Quickbooks?

Each company decides if they would like additional steps, but the accounting cycle typically includes these 8 steps: Identifying transactions. Recording transactions. Posting the general ledger.

What is Step 1 of the accounting cycle?

Step 1: Identify Transactions

The first step in the accounting cycle is identifying transactions. Companies will have many transactions throughout the accounting cycle. Each one needs to be properly recorded on the company's books. Recordkeeping is essential for recording all types of transactions.

What are the 7 steps of accounting cycle?

The Accounting Cycle: The Crucial Steps in the Accounting Process

- Identifying and Analysing Business Transactions. ...

- Posting Transactions in Journals. ...

- Posting from Journal to Ledger. ...

- Recording adjusting entries. ...

- Preparing the adjusted trial balance. ...

- Preparing financial statements. ...

- Post-Closing Trial Balance.

What is the 5 step accounting cycle?

Explaining Accounting Cycle in Context

Defining the accounting cycle with steps: (1) Financial transactions, (2)Journal entries, (3) Posting to the Ledger, (4) Trial Balance Period, and (5) Reporting Period with Financial Reporting and Auditing.

How does the accounting cycle start?

Identify Transactions: An organization begins its accounting cycle with the identification of those transactions that comprise a bookkeeping event. This could be a sale, refund, payment to a vendor, and so on. Record Transactions in a Journal: Next come recording of transactions using journal entries.

32 related questions foundWhich is the correct order of the following steps in the accounting cycle?

The proper order of the following steps in the accounting cycle is: journalize transactions, post to ledger accounts, prepare unadjusted trial balance, journalize and post adjusting entries.

What are accounting cycle?

The accounting cycle is a series of steps starting with recording business transactions and leading up to the preparation of financial statements. This financial process demonstrates the purpose of financial accounting–to create useful financial information in the form of general-purpose financial statements.

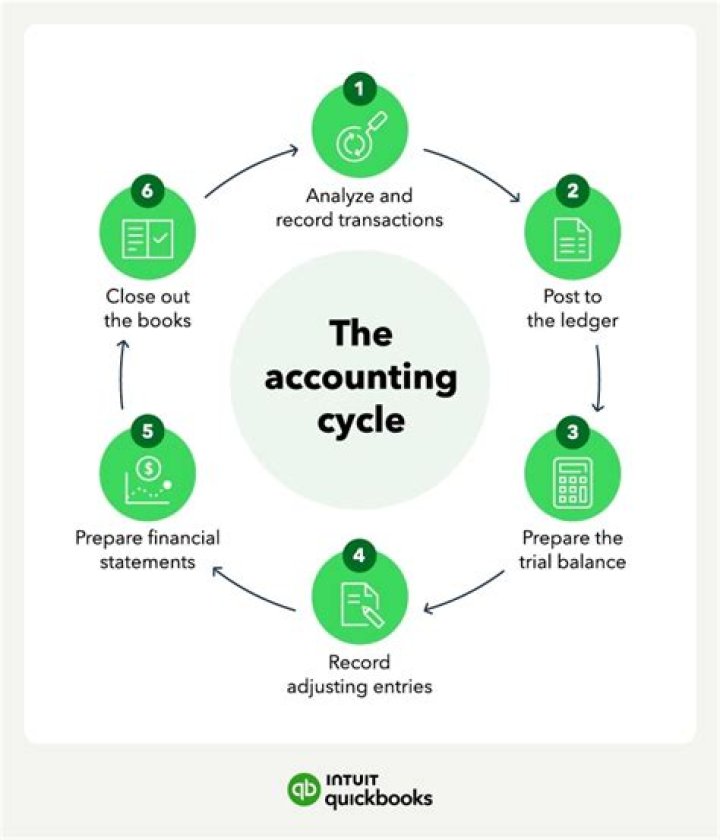

What are the first 5 steps in the accounting process?

- Step 1: Analyze and record transactions. ...

- Step 2: Post transactions to the ledger. ...

- Step 3: Prepare an unadjusted trial balance. ...

- Step 4: Prepare adjusting entries at the end of the period. ...

- Step 5: Prepare an adjusted trial balance. ...

- Step 6: Prepare financial statements.

What are the five transaction cycles?

The Transaction Cycle model is one way to view basic business processes. The purpose of The AIS Transaction Cycles Game is to provide drill and practice or review of the elements that comprise the five typical transaction cycles identified as: revenue, expenditure, production, human resources/payroll, and financing.

What is the accounting cycle 6 steps?

The Six Major Steps of the Accounting Process. The steps of the accounting process are analyzing, recording, classifying, summarizing, reporting, and interpreting. Computers are often used in the recording, classifying, summarizing, and reporting.

What are the 10 steps in the accounting cycle?

10 Steps of the Accounting Cycle

- Analyzing transactions.

- Entering journal entries of the transactions.

- Transferring journal entries to the general ledger.

- Crafting unadjusted trial balance.

- Adjusting entries in the trial balance.

- Preparing an adjusted trial balance.

- Processing financial statements.

- Closing temporary accounts.

What are the 9 steps of the accounting cycle?

Here are the nine steps in the accounting cycle process:

- Identify all business transactions. ...

- Record transactions. ...

- Resolve anomalies. ...

- Post to a general ledger. ...

- Calculate your unadjusted trial balance. ...

- Resolve miscalculations. ...

- Consider extenuating circumstances. ...

- Create a financial statement.

What is the first step in the accounting cycle quizlet?

The first step in the accounting cycle is to analyze business transactions. The second step in the accounting cycle is to prepare a record of business transactions.

What are the 4 steps of the accounting cycle?

First Four Steps in the Accounting Cycle. The first four steps in the accounting cycle are (1) identify and analyze transactions, (2) record transactions to a journal, (3) post journal information to a ledger, and (4) prepare an unadjusted trial balance. We begin by introducing the steps and their related documentation ...

What are the steps in accounting process?

The accounting process is the series of steps followed by the business entity to record the business financial transactions that include steps for collecting, identifying, classifying, summarizing, and recording the business transactions in the books of accounts of the company so that the financial statements of the ...

What is a main transaction cycle?

A transaction cycle is an interlocking set of business transactions. Most of these transactions can be aggregated into a relatively small number of transaction cycles related to the sale of goods, payments to suppliers, payments to employees, and payments to lenders.

What are the two types of cycles in accounting?

There are two different cycles that a small business uses to keep track of its financial status: the accounting cycle and the operating cycle. The accounting cycle records a transaction from the beginning to the end in a ledger.

What are the three cycles of transaction processing systems?

Three transaction cycles process most of the firm's economic activity: the expenditure cycle, the conversion cycle, and the revenue cycle.

What is the last step of accounting cycle?

The last step in the accounting cycle is to make closing entries by finalizing expenses, revenues and temporary accounts at the end of the accounting period. This involves closing out temporary accounts, such as expenses and revenue, and transferring the net income to permanent accounts like retained earnings.

What are the steps of accounting cycle PDF?

10 Steps of Accounting Cycle [Notes with PDF]

- Identification of Transaction.

- Journalizing.

- Posting to Ledger.

- Preparation of Trial Balance.

- Adjusting Entry.

- Adjusted Trial Balance.

- Preparation of Financial Statement.

- Closing Entry.

Which of the following steps comes first in worksheet preparation?

In preparing a worksheet, the following steps must be followed:

- Post Balances in Trial Balance Columns. ...

- Post Adjusting Entries in Adjustment Columns. ...

- Complete Income Statement Columns. ...

- Determine Net Loss or Net Income. ...

- Complete Balance Sheet Columns.

How many steps are in the accounting cycle?

10 Steps of Accounting Cycle are;

Posting from the Journals to General Ledger. Preparing the Unadjusted Trial Balance. Recording Adjusting Entries. Preparing the Adjusted Trial Balance.

What are the steps in the accounting cycle quizlet?

The Accounting Cycle

- Analyze transactions.

- Journalize the transactions.

- Post the journal entries.

- Prepare a worksheet.

- Prepare financial statements.

- Record adjusting entries.

- Record closing entries.

- Prepare a postclosing trial balance.

What are the 3 steps in the accounting process?

The process of going from sales to end-of-month statements has several steps, all of which must be executed correctly for the entire accounting cycle to function properly. Part of this process includes the three stages of accounting: collection, processing and reporting.

Which of the following is the first step in preparing a worksheet quizlet?

The first step in preparing a work sheet includes: - Entering the titles of all accounts and their account number. - Entering the unadjusted balance for each account in the correct Debit or Credit columns of the Unadjusted Trial Balance columns.